Healthcare in the United States already operates at the highest cost in the developed world, and that cost is being absorbed by a workforce whose wages have not kept pace with inflation. Among the lines that have moved within the healthcare cost base, clinician recruitment has moved the fastest and most structurally; it is more expensive in 2026 than in any prior year, such that recruitment costs land at a level the previous decade would not have recognized. We explore how the cost of healthcare recruitment in 2026 is rooted in a structural shortage and exacerbated by a structurally elevated cost environment.

The Cost of a Single Hire, Driver by Driver

The cost of recruiting a bedside clinician in 2026, a registered nurse (RN), for example, is not a single line item. It is ten overlapping cost drivers, each of which has shifted over the past decade. Most have moved up, and none of them have returned to their 2019 baseline. Collectively, they explain why the healthcare recruitment budget is larger in 2026 than it was before the pandemic, and why the gap is structural rather than cyclical.

1. Time-to-fill. The average healthcare recruitment cycle for an experienced bedside RN is 78 days in 2026, down from a pandemic peak of 87 days in 2022, a 2019 baseline of 81 days, and the 82 days in 2015, according to the NSI 2026 National Health Care Retention and RN Staffing Report. Magnet-accredited hospitals, recognized by the American Nurses Credentialing Center as the operational benchmark for high-retention facilities, fill the same roles in 68 days, ten days faster than the national average.

Every day a position remains vacant costs the hospital between $300 and $800 in general units and $900-$2,500 in specialized units, which means a 78-day vacancy gap adds roughly $23k-$195k to the cost of the eventual hire before the new nurse ever starts.

2. Per-separation cost. The fully-loaded cost of losing a single bedside RN averages $60k in 2026, up from $44k in 2019 and $46k in 2022. For context, the 2015 baseline ranged from $37k-$57k. This cost average encapsulates and obscures distinct cost categories, such as vacancy coverage at $300-$800 per day ($23k-$62k over 78 days), separation admin at $2k-$5k per departure, and direct talent acquisition costs, which can be as much as $11k per hire.

3. Onboarding cost. The all-in cost to onboard a replacement RN totals roughly $23k per hire, including clinically non-productive activities such as orientation, as well as facility-specific training and compliance. Comprehensive onboarding is worth it for long-term hires, but as facilities increasingly rely on short-term agency contracts and experience significant first-year churn, aggregate onboarding costs per role with a rotating cast are ballooning.

4. Preceptor drag. A newly permanently-hired RN must complete a 6-12 week clinical preceptorship under a senior bedside nurse. During that period, the senior nurse’s clinical capacity drops by 50% while the new hire operates below 60% of an experienced clinician’s productivity. The dollar cost of that drag averages roughly $7k per hire in 2026, up from approximately $5k in 2019, and the trajectory tracks the rise in senior RN wages rather than any change in preceptorship duration. The 6-12-week duration has stayed flat; the dollar value of the diverted senior hours has not.

5. Agency bill rate. Hospitals paid an average of $90.54 per hour to staffing agencies for travel nurses in 2026, down from a 2022 pandemic peak of $133.47 per hour but still 39% above the 2019 baseline of $65.00 per hour, according to AMN Healthcare’s analysis of travel nurse cost mechanics. The agency markup embedded in that rate, typically 25%-40%, means that $22-$36 of every hour billed goes to the agency rather than the clinician. The 2026 market has stabilized at a structurally elevated level rather than returning to pre-pandemic norms, and the travel nursing sector is projected to hold a $14.3B revenue baseline in 2026.

6. Conversion fees. When a hospital attempts to convert a known-fit agency nurse to permanent status, the agency contract imposes a conversion fee of 15%-25% of the nurse’s first-year salary. With the average annual staff RN salary at $86k, the typical fee lands at $17k per conversion, although some agencies use flat-rate structures of $5k-$15k or time-based sliding scales that penalize early conversion. Three states have moved to restrict or pro-rate these fees: Iowa, effective July 2022; Louisiana, effective August 2022; and Oregon, effective July 2023.

Regardless, the standard contract in most jurisdictions still treats conversion as a revenue event for the agency rather than a retention event for the hospital. The deeper breakdown of how that toll operates is detailed in the conversion fee analysis published in June 2026.

7. Sign-on bonus. The average sign-on bonus for a permanent bedside RN hire reached $18.4k across 127 hospitals in the first quarter of 2026, with standard acute care ranges of $10k-$25k and high-acuity specialty or shift-specific roles reaching $40k. Sign-on bonuses were not a mainstream recruitment tool before 2015; standard bedside postings offered $2k-$5k at the specialty edge. By 2019, the same roles commanded $8k, and by 2022, the average had climbed to $12.5k. The 2026 average is roughly nine times the 2015 figure, and the bonus has shifted from a niche retention tool in healthcare recruitment to a baseline expectation in most permanent RN offers.

8. First-year turnover. Between 22.7% and 29% of newly hired bedside nurses leave their first position within 12 months, meaning the hospital absorbs the full onboarding and preceptor costs and then pays the per-separation costs for the same position within the same fiscal year. The international pipeline is the structural exception, with first-year retention at 94.4%. But for domestic hires, the first-year attrition rate is the single largest multiplier of the per-separation costs.

9. Agency share of nursing labor expense. Contract labor peaked at 39% of total hospital nursing labor expense in 2022, up from 5% in 2019, and the post-pandemic correction has brought the share down to approximately 12%-15% in 2026. That share is still two to three times the pre-pandemic baseline, and the dollars have not come back to the hospital. A higher share of the wage bill is still funnelled to clinicians via an agency and at a higher per-clinician cost.

10. International recruitment fees. Hospitals that engage international healthcare recruitment have two main pathways. The TN (Trade NAFTA) treaty visa, at $7k-$5k per nurse, is the cheaper and faster option, but is restricted to Canadian and Mexican nationals under the USMCA framework, which makes the addressable pool too small to scale for most facilities. The alternative is the EB-3 (employment-based) immigrant visa, which costs an upfront placement fee averaging $55k per nurse as a one-time capital expense, with the typical hospital hiring roughly 28 nurses per cohort for an aggregate fee of $1.5M per active program.

The US has a significant skills shortage in healthcare, and the cumulative effect of these ten drivers is the dollar weight each facility carries into every healthcare recruitment decision. Healthcare recruitment is more expensive in 2026 than it was before the pandemic, and the gap is structural rather than cyclical. In any other industry, a skills shortage attracts more students to study the relevant professions, but such is not the case in US healthcare. To understand the full picture, we must discuss why the supply side cannot flex fast enough to relieve the rising cost pressures, as well as the underlying operating environment and how it is making each driver worse.

Why Not Just Train More Clinicians for Healthcare Recruitment?

Each of the 10 cost drivers above points in the same direction: at a supply side that cannot flex fast enough to relieve the cost pressure. Even if every cost pressure described above were resolved tomorrow, the underlying supply deficit would still be widening, and that is the second half of the problem.

The Domestic Pipeline Bottleneck

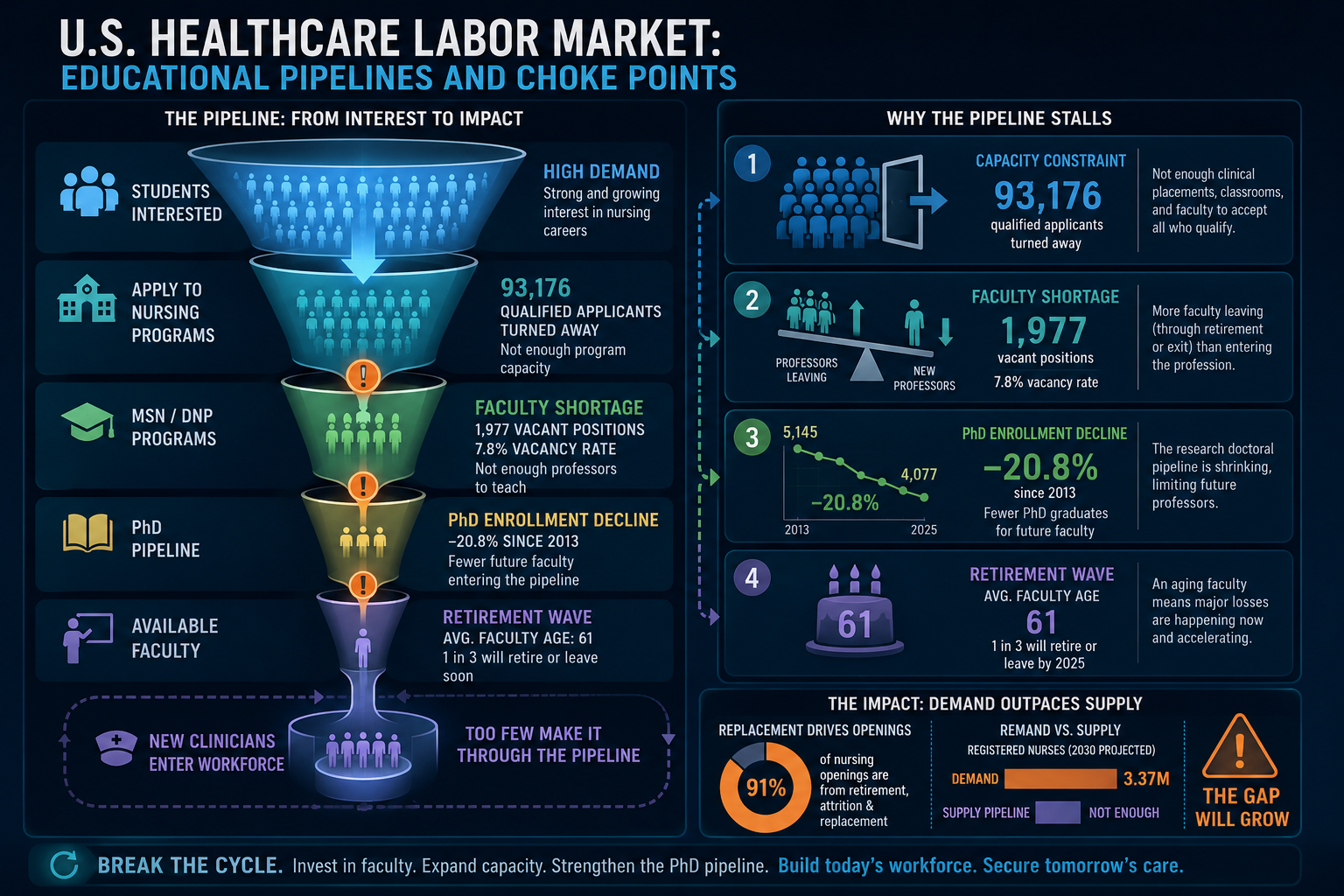

Ironically, interest in nursing is at a multi-year high. Bachelor of Science in Nursing (BSN) enrollment is up 7.6% in the 2025/2026 academic year, with 19,830 additional students entering the pipeline, following a 4.9% increase in 2024 that reversed a brief post-pandemic contraction. The clinician school recruitment function is attracting interest from prospective candidates but failing to convert that interest into seated students.

Such a conversion failure is evidenced in 2025, during which United States nursing schools turned away 93,176 qualified applications, up from 80,162 in 2024 and 65,766 in 2023. Entry-level BSN programs alone rejected 75,255 qualified applicants. The pipeline is widening on the input side while the seat count is held constant by structural ceilings.

The four structural limiters on capacity include:

- a shortage of clinical placement sites,

- faculty vacancies,

- classroom space, and

- budget cuts,

which, combined, caps enrollment regardless of how many qualified applicants apply. The state appropriations cycle that funds expansion takes years, the donor cycle takes years, and the construction cycle that adds classroom and lab space takes years. Even when carefully coordinated, the bottleneck is locked in for a planning horizon longer than any current budget cycle.

Faculty as the Choke Point

While these are mentioned in the previous section, faculty vacancies are worth a closer look. The national full-time nurse faculty (graduate-level instructor) vacancy rate is 7.8%, representing almost 2,000 vacant teaching positions, with regional peaks of 9.8% in the West and lows of 5.6% in the Midwest. Even if institutions had the funding to increase candidate clinician capacity and clinical training slots, these programs cannot expand because the instructors qualified to teach are not in the building. So why not just hire more instructors?

Roughly 8 in 10 of the vacant faculty roles require or prefer instructors with a terminal doctoral degree (the highest level of academic credentials in a specific discipline). At the same time, enrollment in research-focused doctoral nursing programs has declined for eleven consecutive years, contracting by approximately 25% since 2013.

Furthermore, the existing faculty cohort is also approaching retirement fast, with average ages of 61.2 for professors, 55.6 for associate professors, and 49.6 for assistant professors. A 2016 Nursing Outlook study projected that one-third of the active nursing faculty workforce would retire or leave academia by 2025. Basically, the instructors are aging out and not being replaced.

The reason is structural. A senior bedside RN with a BSN and 5-10 years of experience typically earns $80k-110k, and up to $140k-160k with more experience in high-acuity speciality. On the other hand, a nursing instructor with a master’s degree at a community college or state university typically earns up to $85k for a 9-month contract and tops out at about $115k with experience because they operate inside fixed salary bands tied to state budgets. Why teach when you can do and get rewarded more?

Ironically, the clinical workforce the faculty cohort trains has an aging problem of its own.

An Aging Workforce Leaving Faster Than It Can Be Replaced

The median age of registered nurses in the United States is between 50 and 52 years, with nearly 25% of all practicing nurses aged 55 or older, and approximately 40% of active RNs plan to retire or leave clinical practice within the next five years. The replacement arithmetic does not balance even at current graduations, because the exit velocity outpaces the entry velocity regardless of how many new seats the pipeline adds.

Additionally, bedside exit intention has accelerated materially in 2026.

- 43% of practicing nurses indicate a high likelihood of leaving bedside clinical care within the next year, up from 38% in 2025.

- 23% of active nurses plan to leave the nursing profession entirely in the next twelve months, up from 15% in 2025.

- And of those planning to leave the bedside, 16% are absorbed into non-clinical roles such as case management, utilization review, and insurance administration. In fact, as many as 71% of case management personnel exited bedside roles.

The workforce is shrinking at the bedside, even when licensure counts are stable. The international channel is the remaining lever a facility can pull on to replace capacity that the domestic pipeline will not deliver in time. However, even this channel, too, has its issues.

The International Pipeline Throttled by Visa Backlog

International nurses are sponsored under either the EB-3 immigrant visa or the TN treaty visa. EB-3 is the dominant pathway for nurses from countries outside North America, while the TN visa, restricted to Canadian and Mexican nationals under the USMCA framework, provides a faster non-immigrant path with no numerical cap. The two channels are not interchangeable: EB-3 trades speed for permanence, TN trades permanence for speed.

As mentioned in the list of cost drivers, these channels are not costless, but are worth it. Facilities will pay up to $55k to secure an international clinician, which translates to $1.5M for the average hospital cohort (28 nurses). However, the domestic alternative is not a 28-nurse cohort of permanent hires at zero upfront cost; rather, it is a 28-position vacancy cycle that carries 28 per-separation costs and onboarding cycles at $40K-$85K each ($1.12M-$2.38M), 5-7 first-year clinician turnover events, and 78 days of vacancy coverage per role. The international channel may have a 12 to 24-month start-lag but delivers a 94.4% first-year retention rate, making it still worth the investment.

As of 2022, approximately 500,000 EB-3 immigrant nurses were practicing in the United States, representing about 16% of the 3.2 million RN workforce, according to the Health Resources and Services Administration workforce analysis. That figure is the cumulative base the EB-3 channel has delivered rather than the annual flow. The EB-3 channel has been working for decades; what changed in 2026 is the queue, not the channel itself. Nava’s EB-3 vs TN comparison walks through the two pathways, and Nava’s international recruitment documentation details the cohort-based execution model the EB-3 path uses to deliver permanent residency from day one, but the underlying queue constraint is what limits the EB-3 program to single-cohort delivery rather than continuous flow.

The annual cap of roughly 40,000-50,000 EB-3 visas (after rollover from unused EB-1 and EB-2 slots) is shared across all EB-3 employment categories, not just nurses, and a 7% per-country limit further constrains the volume any single country can send. The actual binding constraint is the queue, not the cap. As of July 2026, the Philippines sits at a two-year backlog and India at a twelve-year backlog. The channel is open on paper and closed in practice for the countries that supply most of the pipeline. Meanwhile, on the domestic side, a different supply distribution problem is taking shape that does not require any nurse to leave the profession for the system to lose access to skilled workers.

Geographic Reallocation of the Clinical Workforce

Two equivalent roles, same pay, same work – if one city costs 20% less in housing, the clinician moves. That is the decision the General Services Administration (GSA) stipend structure is forcing on the bedside workforce in 2026. Agency nurses who receive a housing stipend decide how much of that allowance they are willing to spend on rent, and securing cheap or shared accommodation to create a tax-free surplus can be a reliable source of significant additional income.

For example, GSA per diem daily lodging rates in Florida for 2026 ranged from $110 to $436 (Key West, March, 2026), depending on the city or county and the time of the year. Acquiring accommodation that costs just $50 less per day than the stipend translates to $18k of tax-free annual income.

However, as the GSA stipend ceiling has met local rental market rates in high-demand cities, such as Boston, San Francisco, and New York. The tax-free surplus that the stipend was designed to deliver has become a shortfall in those metros. The shelter index rose 3.4% over the preceding twelve months, and short-term landlords on furnished rental platforms raised their weekly rates to match the cap, accelerating the reallocation.

The consequences of clinician migration fall on the facilities that need it most. The same clinicians who would have staffed those metros a year ago are now working the higher-billing secondary or rural assignments instead, and the contract agencies that place nurses in the metros are raising the rates they bill the safety-net hospitals to recruit the same clinicians back into the cities.

The international channel is open, but the queue is closed. The 140,000 cap is not the binding constraint. The per-country backlog is, and the countries that send the most nurses are the ones that wait the longest.

The Cost Shock: Tightening the Margin

The cost side of running a hospital in 2026 has changed in ways that have nothing to do with recruitment on the surface, but everything to do with it on the budget. Energy, housing, and fuel costs all moved in 2026 in magnitudes that the hospital’s fixed-reimbursement revenue base cannot match. The result is a margin compression that lands on the staffing line, the same line the recruitment function depends on.

Energy Overhead That Cannot Scale Back

In May 2026, energy costs in the United States were up 23.5% over the previous year, with electricity up 5.9% and natural gas up 3.0%. For a typical hospital, utility costs run about 1%-3% of the operating budget, and that share can reach 10% in large teaching hospitals with intensive HVAC and infection-control demands. The hospital’s revenue did not increase to match energy cost hikes, meaning the additional expenditure must come straight off the bottom line. However, when on thin margins and the bottom line has no wiggle room, organisations generally tend to take measures to reduce their variable costs, in this case, their energy usage.

Yet, a hospital cannot renegotiate the regulatory floor it operates on the way a commercial property can renegotiate a lease, because infection control, MRI cryogenics, electronic health record uptime, and patient safety do not tolerate a power-down cycle. So, when the energy bill goes up, the next inflexible cost line gets compressed, and the supply chain that delivers the medical supplies is one of them.

Fuel Surcharges and the Hidden Transport Line

A 60% surge in wholesale diesel and gasoline prices drove immediate fuel surcharges of 8%-12% across logistics operations. That translated into real dollar overhead on routine clinical movement, and the hospital cannot cut those expenses any more than it can cut the electricity, because specimen integrity, temperature-controlled drugs, and surgical transfers do not tolerate a postponed run. Ambulance and emergency medical services providers face the same surcharge but are funded by a Medicare ambulance fee schedule that has not adjusted for fuel costs since 2002.

Furthermore, the medical supplies on which facilities rely are rarely sourced on-site. Facility suppliers are not bound to predetermined reimbursements and are free to pass on variable costs to their clients and customers. If the fuel and production costs go up, their prices go up. Essentially, the increase in fuel surcharges is an unrecoverable expense in the short and possibly medium run. The gap between the logistics cost base and the reimbursement base will be absorbed by the facilities and EMS operators until the fuel provisions come up for review. Even if adjusted timeously, those adjustments may not account for cost-push (supply-side) inflation.

The Impact of Rising Variable Costs on Recruitment

Energy, logistics, and medical supplies are inflexible inputs. If a facility is to remain operational, some corners cannot be cut; there is an uncompromising line between compliance and licenses getting revoked. But there are significant grey areas and flexible solutions when it comes to clinical personnel. So when variable costs rise on a fixed reimbursement base, the staffing budget is where the margin compression hits, because it is the largest controllable expense on a hospital balance sheet. Hence, the reliance on agency clinicians, which, in the face of higher demand, results in agencies billing higher rates to facilities, offering higher hourly wages to talented clinicians, and ultimately luring more clinicians away from permanent placements.

Fixed reimbursement absorbs rising costs on the margin line. The staffing budget pays for energy and fuel that it was never budgeted to accommodate.

Why Reactive Recruitment Cannot Fix This

A structurally tight supply of clinical skills and a structurally more expensive variable cost base combine to produce one predictable response in terms of staffing decisions:

- Defer investment in sustainable recruitment systems, use agency staffing to cover the gaps, and absorb the relatively smaller agency premium until conditions improve, and

- Only when the need can no longer be ignored should the facility move for permanent placement.

We call this Reactive Recruitment.

The published research on staffing cost curves, on premium labor versus permanent retention, and on reactive onboarding economics each tells the same story. Reactive recruitment does not just fail to solve the problem; it is a negative feedback loop that actively accelerates it. Nava’s earlier analysis of why reactive recruitment fails in healthcare staffing documented the same trap in the pre-2026 cycle, and the math has only hardened since.

The Non-Linear Cost Curve Past 10% Vacancy

Below 10%, facilities can rely on overtime to fill the gaps. The additional costs are predictable, and this is a viable solution for short-term gaps. Once a facility’s permanent vacancy rate crosses the 10% threshold, most facilities must acquire coverage externally, and the external price has its own escalation curve. The facility enters the non-linear regime at the moment it most needs the cost curve to be linear, driven by compounding mechanisms in the form of a burnout-attrition feedback loop in which rising patient loads accelerate voluntary departures among remaining staff, and agency cost penalties that force facilities to raise hourly bill rates to attract scarce contingent labor.

Calibrated behavioral economic models published in peer-reviewed research confirm that unrestricted hospital spending on agency nurses reduces immediate staffing gaps but raises long-term labor costs. The premium wages paid to contract labor divert funding away from permanent retention, which lowers morale among the permanent staff and further destabilizes the core workforce. The premium itself becomes an agency recruitment message to the workforce the facility is trying to retain, because the same dollar that fills a vacancy also signals to the permanent staff that the contingent rate is the real market.

Why Agencies and Sign-On Bonuses Accelerate the Increase

When a facility raises its agency bill rate or posts a large sign-on bonus to close a vacancy, the wage signal reaches the existing permanent staff at the same time it reaches the external market, and the gap between premium contingent pay and standard permanent pay widens into a visible comparison the permanent workforce can act on. The facility is broadcasting both an external recruiting message and an internal retention test at the same time, and the two messages are in direct conflict. The instrument the operator reaches for first is the same instrument that erodes the workforce it is trying to protect.

Experienced permanent clinicians respond to that wage signal by converting to travel or per-diem contracts, where the blended hourly rate (including tax-free stipends) materially exceeds their employed compensation. Consequently, the facility that paid the premium to fill one vacancy ends up with two: the original opening plus the new opening left by the clinician who left permanent status. The premium buys its own replacement, and the budget cycle absorbs both openings at the same time, on the same line. The facility ends up paying for the same coverage it would have paid for without the premium, and the dollar overhead now sits on a workforce that is also smaller than it was before the premium was offered.

Reactive Recruitment Is Transactional, Not Strategic

Reactive recruitment is transactional, not strategic. The model pays for every resignation twice – first to lose the nurse, then to onboard the replacement – and treats each vacancy as an isolated event rather than a predictable line in the budget cycle. A system that hires only after a resignation has occurred is structurally incapable of building a pipeline, which means it will pay a rising premium for scarce labor in every future budget cycle. A transactional function cannot solve a structural shortage, because a transactional function is designed to fill openings rather than to build a pipeline. The cost drivers in H2.0 are the symptom; the model that produces them is the cause.

A reactive hiring model is a churn model with hiring bolted on. It pays four lines on the same event, every event, forever.

The structural alternative is documented in Nava’s travel-to-permanent analysis, which walks through how a facility that already runs the most thorough hiring evaluation in healthcare (the 13-week contract) can convert the highest-performing clinicians already on the floor and bypass the agency billing loop entirely.

Conclusion

What does the alternative look like? The responses that actually work sit at three layers.

At the policy level, the bipartisan Healthcare Workforce Resilience Act, reintroduced in late 2025, proposes to recapture up to 40,000 unused employment-based green cards from fiscal years 1992 through 2024 and allocate 25,000 of them to professional nurses, while the H-1Bs for Physicians and the Healthcare Workforce Act (H.R. 7961, introduced April 2026) seeks to exempt healthcare workers in direct patient care from prevailing fee hikes and standard lottery caps.

At the facility level, structural investments in formal nurse residency programs and clinical ladder programs have been shown to reduce first-year attrition from roughly 1-in-3 to under 1-in-10, and to cut turnover among ladder-completing clinicians to 4.20% against 14.09% for the broader population. However, most facilities cannot afford such a program in-house, and even when the budget allows, there is a lack of clinical-educator bandwidth and preceptor depth.

A more sustainable approach is to abandon reactive recruitment and start building relationships and candidate pipelines before the need becomes urgent. Having an extra RN or two on the roster is financially, operationally, and clinically better than hosting a rotating cast of agency nurses contracted during peak demand. However, individual facilities are often ill-equipped to retain the expertise and clinician network required to maintain a pipeline of fit and culturally-vetted candidates that the facility itself is already short on. Hence, the need for a strategically aligned recruitment partner.

At the recruitment-partner layer, the recruitment function has to be rebuilt as an embedded ally inside the facility’s workforce plan rather than a vendor that activates at the point of resignation. The structural alternative is an operating model that performs that role across the full clinical workforce, incentivised to alleviate the financial pressures of agency reliance, rather than exacerbating them.

A structural alternative has to perform three connected jobs, and the connection is the point. They should:

- Be capable of identifying talent that would be fit for your environment and culture; clinicians whose preferences and individual characteristics are such that they, too, would be professionally comfortable operating within your facility. This meticulous match-making, resource-intensive as it may be for a recruitment partner, is an approach that all but guarantees minimal clinician churn.

- Possess the means to convert existing agency staff proven to be effective within your facility into permanent staff. Returning agency nurses who have seamlessly integrated into your units and developed lasting team dynamics may prefer to work at your facility, but are bound by agency contracts, just as the facility itself is restricted by costly conversion fees. An effective partner bridges these barriers to create effective professional partnerships.

- Facilitate the addition of qualified international clinicians to your ranks. As discussed, the skills shortage is cultural, and no short-term solution is in sight. Facilities may continue to scramble for talent in the local market, but international cohorts have been effective in alleviating labour market pressures.

For facilities still running on a reactive model, the 10 cost drivers discussed are the symptoms, the model that produces them is the cause, and structural changes required at the policy level are beyond a single organisation. The most viable paths forward to hedge against rising recruitment costs are to initiate a long-term residency solution for graduate candidates when possible and to engage a strategic partner focused on sustainable solutions. The choice between transactional placement and permanent pipeline is no longer philosophical; it is fiscal.